Managing cost, performance and progress is one of the most important responsibilities of a project manager. In practice, this is usually one of the areas that receive a lot of attention by project sponsors, steering committees and other stakeholders, given that the budget is often one of the relevant constraints of a project.

Despite its importance, it happens that project managers and PMOs struggle with the holistic implementation of Earned Value Management. If you are preparing for your PMP certification exam, you will find that Earned Value Analysis (EVA) is a technique many candidates are also worried about. In this article, we are going to provide you with a comprehensive overview of Earned Value Management (EVM), supplemented with links to in-depth articles on the related methods.

What Is Earned Value Analysis (EVA) in Project Management?

Earned Value Analysis (EVA) is a technique used in project management for monitoring and controlling purposes. Several processes of the PMI methodology refer to this technique (read more below) which belongs to the data analytics group of techniques (source: PMBOK®, 6th edition, part 1, ch. 4.5.2.2, p. 11).

The main indicators of the Earned Value Analysis technique are

- Earned Value (EV),

- Planned Value (PV),

- Actual Cost (AC) and

- Budget at Completion (BAC).

We will cover these measures in detail in the next section.

The indicators can be calculated for a single period or cumulative for multiple periods as well as for the entire project or parts of it (e.g. work package- or control accounts-level).

Some authors include variance and trend analyses in the definition of EVA. Others use EVA and EVM synonymously. This article however follows another common interpretation that groups these methods under Earned Value Management (refer to the next section for details).

What Is Earned Value Analysis Used for?

The goal of the earned value analysis is to support and facilitate the control cost process. The results of this analysis are used for Earned Value Management (EVM) which analyses variances, trends and forecasts based on the EVA results. Read more about these uses in the EVM section below.

For projects following the PMI methodology, Earned Value Analysis is a suggested technique of the following processes:

- Monitor and Control Project Work,

- Control Schedule,

- Control Costs, and

- Control Procurements.

What Is Earned Value Management (EVM)?

Earned Value Management is defined as a methodology for measuring project performance in a comprehensive and holistic way. EVM focuses on the measurement of costs, schedule and scope against the project baseline. The PMBOK® specifies this baseline as the performance measurement baseline that consists of the cost baseline, the scope baseline, and the schedule baseline.

The measures and indicators used in EVM include

- the EVA indicators,

- variance analysis,

- trend analysis, and

- forecasting.

Refer to the next section for the indicators of the Earned Value and Variance analyses and forecasting, incl. their formulae.

Thus, the earned value management provides a holistic view on where the project stands in terms of scope, budget and schedule. This processing makes deviations from the project plan and budget transparent. This allows project managers to identify and take necessary action.

What Is Earned Value Management Used for?

Although not explicitly set out in the PMBOK®, Earned Value Management is in practice often also used as a reference to the recurring process of measuring project progress and performance.

The individual set of measures and the form and level of detail of Earned Value Management is typically set out in the schedule management plan and in the cost management plan of a project. This includes the granularity, reference objects, and tracking methods, for instance. These requirements are individually defined for each project.

EVM may include and trigger, for instance, the following sample steps and processes (non-exhaustive; note that these steps may be part of separate processes in PMI methodology):

- gathering the data needed for EVA, variance and trend analyses as well as forecasting,

- performing the calculations,

- interpreting the results,

- initiating further investigations, e.g. a root cause analysis for variances,

- identifying (and, subsequently, taking) actions, if necessary,

- communication with stakeholders, and

- re-planning, initiating a re-estimate, agreeing on steps and resolutions with stakeholders.

EVM results are typically part of the regular status reporting – often in aggregated or color-coded form rather than in detail though.

For further details on the use of Earned Value Management in the PMI framework, refer to the PMI Practice Standard for Earned Value Management.

A supplemental approach to EVM is Earned Schedule Management which focuses on the measurement of schedule variances and trends separately from the value and cost performance (source: PMBOK®, 6th edition, p. 233).

The EVA / EVM Measures and How They Are Calculated

Earned Value Analysis Measures

The Earned Value Analysis comprises the indicators

- Earned Value (EV),

- Planned Value (PV),

- Actual Cost (AC) and

- Budget at Completion (BAC).

Planned Value (PV)

The planned value is the share of the budget (excluding management reserve) assigned the activities or periods in the scope of the analysis.

Earned Value (EV)

This indicator measures the progress of the project. Its value is the sum of the budget planned and authorized for the work that has already been completed.

Actual Cost (AC)

The AC refers to the cost incurred for the work performed.

Budget at Completion (BAC)

The total budget represents the authorized value (and the sum of estimated cost) of the scope of a project at completion.

Variance Analysis

The Variance Analysis consists of these indicators:

- Cost Variance (CV),

- Schedule Variance (SV),

- Variance at Completion (VAC).

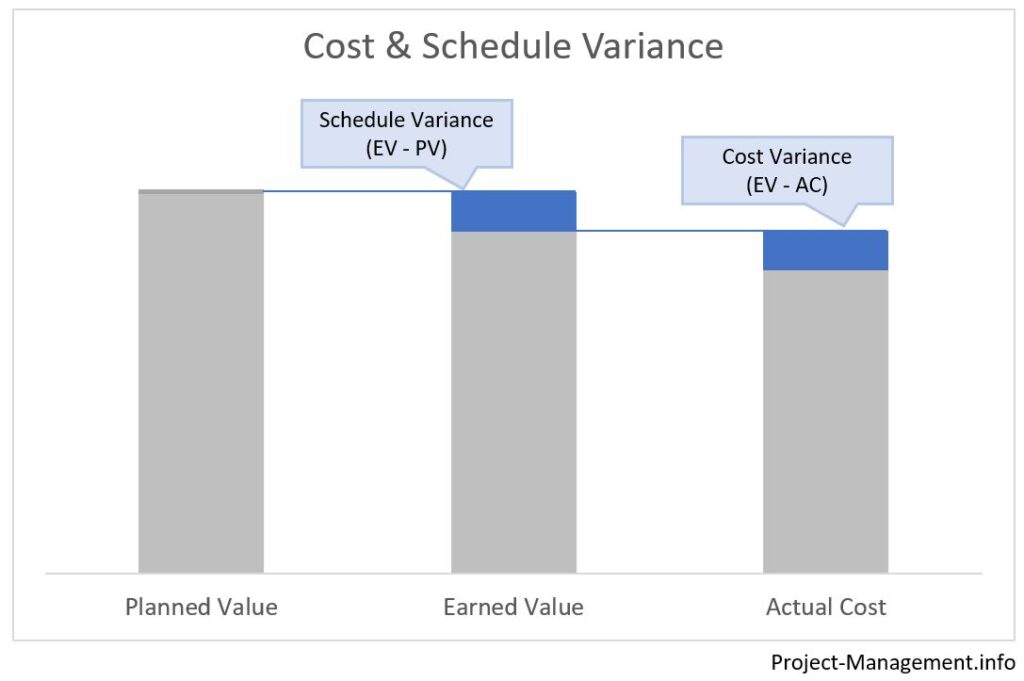

Cost Variance (CV)

Definition

The cost variance indicates the difference between the earned value and the actual cost. If the earned value exceeds the actual cost, the cost variance has a positive value (and the other way around).

Formula

CV = EV – AC

Schedule Variance (SV)

Definition

The schedule variance compares the earned value with the planned value for the respective period. A positive value indicates that a project is ahead of the plan.

Formula

SV = EV – PV

Variance at Completion (VAC)

Definition

The variance at completion refers to the difference between an initially authorized budget (BAC) and an authorized estimate at completion (EAC).

Formula

VAC = BAC – EAC

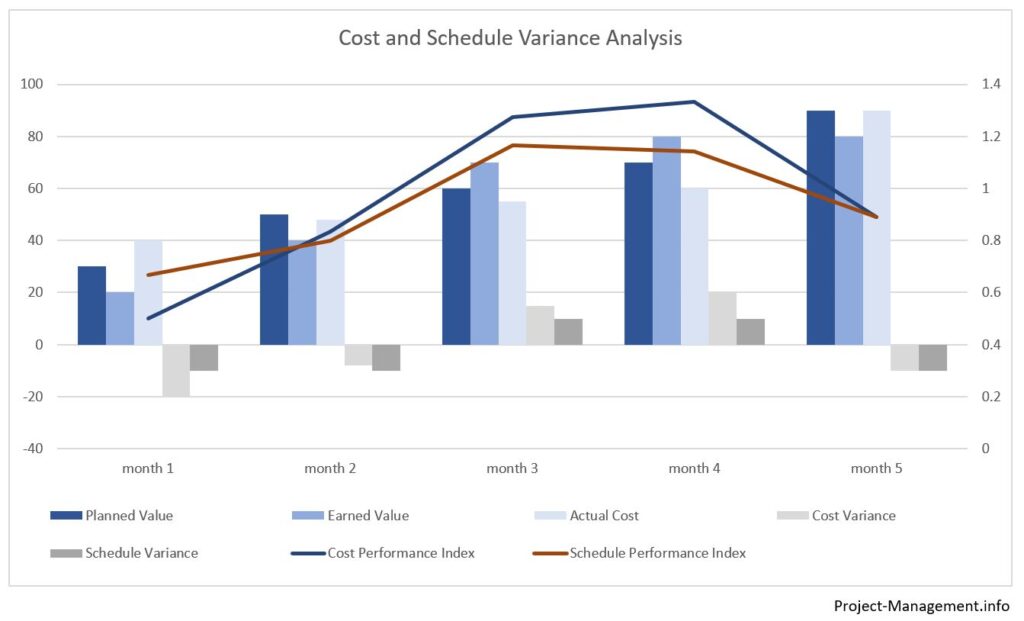

Cost Performance Index (CPI)

Definition

The cost performance index represents the corresponding variance as an index value. A value of 1 indicates that the earned value meets the actual cost while a value below 0 occurs when cost exceeds the earned value.

Formula

CPI = EV / AC

Schedule Performance Index (SPI)

Definition

Similar to the CPI, the schedule performance index compares the earned value with the planned value. If its value is 1, the project is on track. A value below 1 indicates that the project is behind schedule.

Formula

SPI = EV / PV

Forecasting

The forecasting techniques consist of:

- Estimate at completion (EAC),

- Estimate to Complete (ETC), and

- To-Complete Performance Index (TCPI).

Estimate at Completion (EAC)

Definition

The amount of total cost that is expected for the completion of the project. If a new estimate has been accepted by the project, the EAC replaces the

Formula

EAC = AC + ETC

Where ETC = Estimate to complete.

There are different ways to determine this estimate, which are introduced in the following section.

Estimate to Complete (ETC)

The ETC is the difference between the current cumulative actual cost and the estimate at completion. It can be determined based on the CPI and SPI or through a re-estimation of the remaining amount of work.

Read more details and find the formulas in our detailed article on EAC and ETC.

To-Complete Performance Index (TCPI)

The TCPI calculates the future cost performance that would be required to complete the work within the budget.

Read more in our detailed article.

Conclusion

Every project needs to manage schedule, cost or scope requirements and restrictions. Earned Value Management is a comprehensive yet not over-sophisticated methodology that allows project managers to measure and monitor the performance of a project.

Thereby, the Earned Value Analysis focuses on the measurement of cost and value. The Variance Analysis assesses the differences between the project baseline(s) and the actual performance. Forecasting is used to estimate the future performance of a project and identify the areas of improvement. Trend analysis, on the other hand, refers mainly to the development of variances over different periods.