Estimating cost is an important process in project management as it is the basis for determining and controlling the project budget. Costs are estimated for the first time at the beginning of a project or even before a project has started. Subsequently, the (re-)estimation of the project cost is repeated on an ongoing basis to account for more detailed information or changes to the scope or timeline.

For instance, if the earned value management measures that are used for controlling project cost indicate significant variances from the budget, a re-estimation of the cost and schedule and a revisiting of the overall budget can be inevitable.

The methods introduced in this article are tools and techniques of the “Estimate Costs” process that is part of PMI’s Knowledge Area “Project Cost Management” (see PMBOK®, 6th edition, ch. 7.2).

What Is a Cost Estimate?

A Cost estimate is a quantified expectation of how many resources are required to complete a project or parts of a project.

Such cost estimates are often expressed in currency units. However, other units such as man-days can also be used if the currency amounts are not applicable or irrelevant.

There are different types of cost estimates. The Project Management Body of Knowledge lists the rough order of magnitude (ROM) and the definitive estimate. Both types differ in respect of their accuracy, the project phases in which they are used as well as the available tools and techniques. Some projects use additional, sometimes industry-specific types of estimates.

Cost estimating involves different tools and techniques which typically include

- Expert judgment,

- Analogous estimating,

- Parametric estimating,

- Bottom-up estimating,

- Three-point estimating, and

- Cost of quality.

Read on to learn the details of these techniques, supplemented with examples and practical considerations.

What Are the Types of Cost Estimates?

According to the PMBOK®, there are 2 types of cost estimates:

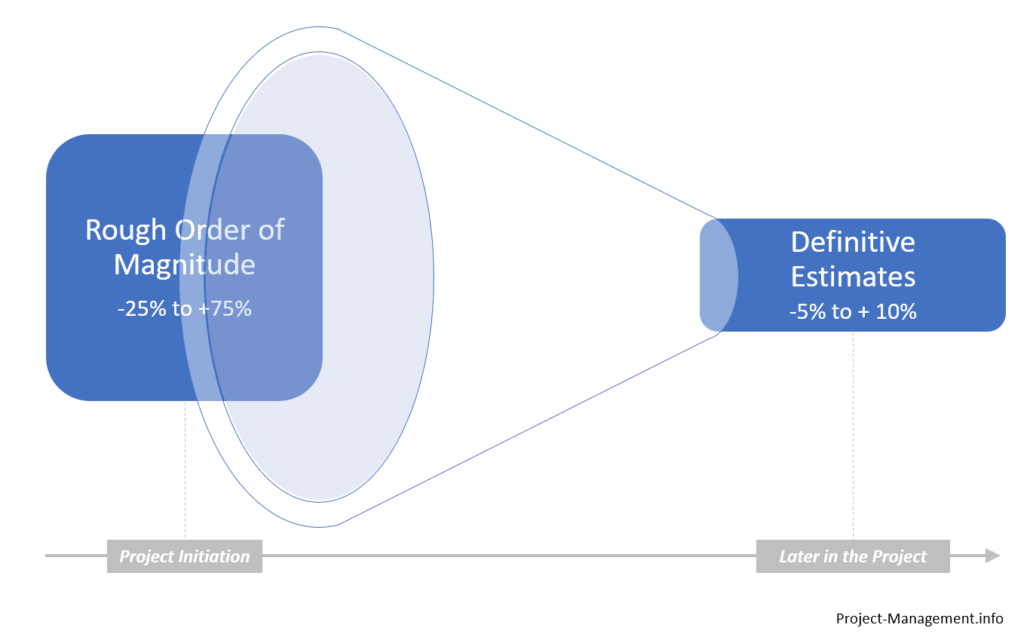

- Rough order of magnitude (ROM) with an accuracy of -25% to + 75% (other frameworks quote a range of +/-50%) and

- Definitive estimate with an accuracy range of -5% to +10%.

Some sources also list so-called preliminary estimates and budget estimates as further gradations of estimate types. There are also industry-specific types of estimates such as design and bid estimates in construction projects (source). However, the current PMI project management framework only refers to the 2 above-mentioned types.

If the budget has to be revisited part way through a project, a so-called estimate to complete (ETC) is determined.

Rough Order of Magnitude vs. Definitive Estimate

The obvious difference between these 2 types of estimates is the accuracy: the ROM is rather inaccurate with a broad range of possible outcomes. It is therefore typically used in project initiation phases where a ballpark figure is sufficient to get a project started.

The definitive estimate is determined in the course of the project when more information and resources for accurate estimates are available.

Read this article for more details on the ROM and the differences between ROM and definitive estimate.

Estimate to Complete (ETC) and Estimate at Completion (EAC)

If partway in a project it turns out that the budget baseline (based on previous estimates) cannot be met, a re-estimation of the project cost is required.

This is done by determining an estimate to complete (ETC) which is used to calculate a new estimate at completion (EAC) that replaces the initial budget at completion and thus becomes the new cost baseline of a project.

When Are Cost Estimated?

Costs are estimated at different points in time throughout the project. The PMBOK states that the process is performed “periodically throughout the project as needed” (source: PMBOK®, 6th edition, ch. 7.2).

The first point to estimate cost is during the initiation phase, e.g. when the project business case or the project charter is created. For these documents, a project manager has to determine the amount of resources that is required to complete the project.

As the information that is available at that point is usually not very detailed, the project manager will likely end up producing a rough order of magnitude estimate rather than a definitive estimate. Later in the project when more information is available, this order of magnitude estimate will be replaced with a definitive estimate.

After the project initiation phase, the cost will be re-assessed during the planning phase, using the techniques introduced in this article.

In subsequent phases, costs are typically (re-)estimated if relevant new information and details become known or if changes to the project scope or timeline occur. One of the common reasons for re-estimating cost is, for instance, when the indicators of the project controlling suggest that the original budget baseline cannot be met.

Why Is Cost Estimation Important in Project Management?

Estimating costs is one of the core activities of project management and planning. This is because a project is defined as being subject to at least three fundamental constraints: scope, budget and time. Cost estimates are obviously addressing the budget constraint; hence they are highly relevant for the management of a project. The initial rough cost estimate is usually included in the project charter as well as in the business case of a project.

The estimation of costs is also necessary to compute the project budget which is subject to the approval of the project sponsor(s). In fact, the process “determine budget” uses a technique called “cost aggregation” which directly refers to the outputs of the “estimate cost” process.

Cost estimates are the basis for allocating budget to work packages and deliverables which can be politically sensitive within a project as well as among its stakeholders. Therefore, budget determination and assignment require some stakeholder involvement, communication and, in many cases, their approval.

In addition, cost estimates are input parameters for the earned value and variance analyses as well as forecasting of project costs.

Tools and Techniques for Estimating Project Cost

This section provides an overview of the tools and techniques for estimating project costs. These methods refer to chapter 7.2.2 of PMI’s Project Management Body of Knowledge.

Click on the links to the detailed articles on these techniques to find further explanations and practical examples.

Comparison of Estimation Techniques

This table compares the approaches to estimating project costs and highlights the differences between these techniques.

| Expert Judgement | Analogous Estimating | Parametric Estimating | Bottom-up Estimating | Three-Point Estimating | Cost of Quality | |

| Input Data | Expertise and experience of the experts | Historic or market data: Values of previous similar projects | Historic or market data: Parameters and values of similar projects | Scope of work, activities | Estimation techniques | Several |

| Method | Experts estimate the resources needed to complete the work in scope, either as a top-down or a bottom-up estimate | Adoption and adjustment of historic values for similar types of work (top-down) | Using the historic cost per parameter unit to determine the expected cost of the current project | Estimating cost at a granular level of the work breakdown structure and aggregating the resource requirements for the whole project or parts of a project | Three-point cost estimates (optimistic, pessimistic and most likely) are determined using one of the previously mentioned techniques, that are then transformed into a weighted average (based on triangular or PERT/Beta distribution) | Although cost of quality is not a generic estimation technique on its own, it can provide input for the other estimation techniques. It involves determining the cost of conformance with certain quality standards compared with the cost of non-conformance and the long-term effects of short-term cost savings |

| Output Type | Several | Cost estimate per activity or project | Cost estimate per activity or project | Cost estimate per activity or project | Refined cost estimate and standard deviation of estimates | Estimation of cost of quality |

| References | PMBOK®, ch. 4.1.2.1 | PMBOK®, ch. 6.4.2.2, ch. 7.2.2.2 Article incl. example; 5-step guide | PMBOK®, ch. 6.4.2.3, ch. 7.2.2.3 Article incl. example | PMBOK®, ch. 6.4.2.5, ch. 7.2.2.4 Article incl. example | PMBOK®, ch. 6.4.2.4; Article Calculator | PMBOK®, ch. 7.2.2.6, ch. 8.1.2.3 Article incl. example |

Expert Judgment

This technique is suggested by the PMBOK (ch. 4.1.2.1) as a way to produce a cost estimate.

If you or your team have experience with the kind of work that is in the scope of a project, you can use expert judgment to produce an estimate. This requires a certain level of familiarity with the subject of a project and its environments such as the industry and the organization.

Expert judgment can be applied to both bottom-up and top-down estimating. Its accuracy depends greatly on the number and experience of the experts involved, the clarity of the planned activities and steps as well as the type of the project.

Two examples of expert judgment are:

- Estimating the rough order of magnitude at the beginning of a project. At that time, estimates are often performed top-down due to a lack of team members. more accurate estimation techniques (such as parametric estimating) may also not be available due to a lack of data.

- (Re-)estimating the efforts needed to generate the deliverables of a work breakdown structure (WBS) by asking those responsible for work packages and activities to estimate their resource requirements. This type of expert judgment can lead to comparatively accurate results.

Besides being an estimation technique on its own, expert judgment is also inherent to the other estimation techniques. For instance, if the comparability of previous work and the current project is assessed or adjustments to parametric estimates are determined.

Analogous estimating

Analogous estimating refers to the use of observed cost figures and related values in previous projects (or portions of a project). In order to be accurate, the type and nature of these reference activities must be comparable with the current project.

“Analogous estimating, also called top-down estimating, is a form of expert judgment.”

Source: Heldman, Kim. PMP: Project Management Professional Exam Study

This technique uses historical data in the form of values and parameters to determine the expected resource requirements of a current project. The historic values are adopted for the current work and can be adjusted for differences in scope or complexity. Analogous estimating is categorized as a gross value estimating approach.

In general, analogous estimates are used if a project has access to historical data on similar types of work while the details and resources for more accurate estimates in the current project, such as parametric or bottom-up estimating, are not available.

Parametric estimating

Parametric estimating is a statistical approach to determine the expected resource requirements. It is based on the assumed or proven relationship of parameters and values. Simple examples are the building cost per square foot in construction projects or the implementation cost per data field in IT projects.

If, for instance, the cost of implementing a new data field in an IT system were $20,000 according to historical data, and a project required 15 new data fields, the total cost of this part of the project would be 15 x $20,000 = $300,000.

The input data can be obtained from previous projects or external data sources such as industry benchmarks or publicly available statistics.

In practice, this technique is employed with a broad variety of sophistication and accuracy. It can be used with a simple ‘rule of three’ calculation but also in conjunction with a complex statistical or algorithmic model that may consider multiple quantitative and qualitative parameters for detailed regression analyses.

In projects that do not use an explicit statistical correlation analysis, some expert judgment is required to assess whether it would be reasonable to apply the historic parameters to the current project. Complexities of projects and activities vary and may therefore require certain adjustments.

For instance, building a highway in a mountainous region likely produces a higher cost per mile than in a flat area. IT development projects in complex IT architectures or systems tend to require more resources than a less complex environment.

Another consideration concerns the expertise and experience of the project team. If a previous project was delivered by highly skilled and experienced resources while the current team is just at the beginning of its learning curve, using unadjusted historic data may understate the estimated cost.

Similar to analogous estimates, adjustments can be made to adapt the parametric estimates to the current project.

Depending on the quality of the input data and its applicability to the current type of work, the parametric estimation technique can produce very accurate figures. However, the higher the accuracy desired the more resources are needed to perform the data gathering and statistical analyses.

Bottom-up estimating

Bottom-up estimation refers to a technique that involves estimating the cost at a granular level of work units. The estimates for all components of a project are then aggregated in order to determine the overall project cost estimate.

In practice, these estimates are often performed at the lowest level of the work breakdown structure (WBS), e.g. for work packages or even activities.

While there is no clear rule on who should be performing this estimation, it seems to be a good practice in project management: asking those project team members who are operationally in charge of the respective work packages or activities to estimate there on work.

Thus, this approach to estimating costs often comes with significantly higher accuracy than top-down estimations. However, obtaining and aggregating these granular estimates normally requires some resources and can potentially become a political challenge, especially in large or complex projects.

Three-point estimating

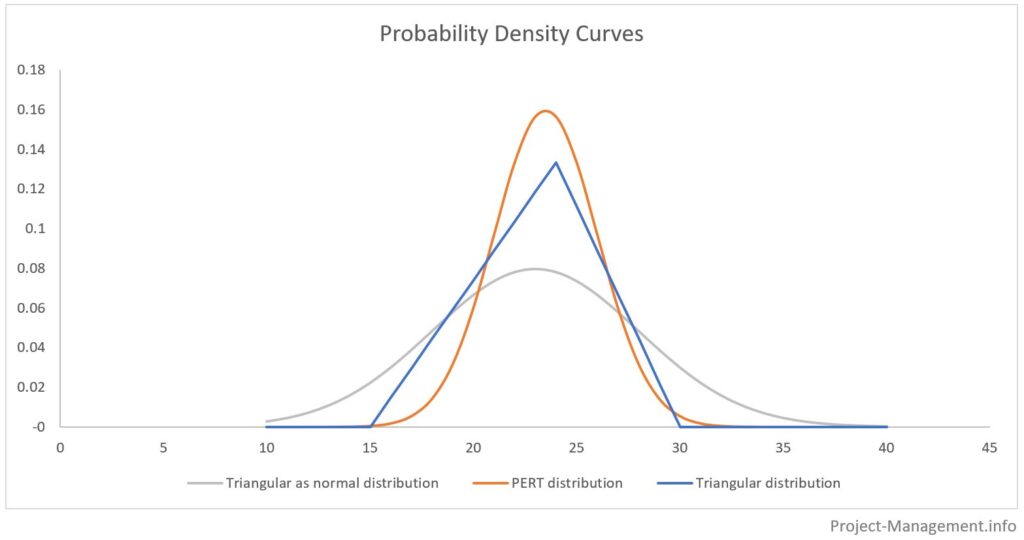

Three-point estimating is a technique that usually leverages on bottom-up estimates, analogous or expert estimates. The concept requires three different points of estimates: the optimistic (best case), pessimistic (worst case) and the most likely cost estimate.

Based on these 3 points, a weighted average cost estimate is determined that overweighs the “most likely” point. This can be done by assuming a triangular distribution, a PERT or beta distribution.

Read this article for further explanation and examples of this technique.

Conclusion

In this article, we have discussed the techniques of cost estimating as suggested by the PMBOK. Note that the level of detail and granularity of the estimates usually increases throughout the project.

In the initiation phase, the rough order of magnitude (ROM) is often the only type of estimate that can be obtained. Definitive estimates will usually require techniques such as analogous, bottom-up and parametric estimating that may only become available in later stages of a project.

Parametric and bottom-up estimates are usually the techniques that provide the most accurate cost projections. They are commonly used if the budget needs to be revisited and replaced with a new estimate at completion.

When a budget is determined and approved, earned value analysis and variance analysis help project managers control the cost and value generated in a project. You will find more details on the measures and the techniques in this article.